“I’ve Heard Enough”: Breaking Down What UP's Kenny Rocker Is Actually Saying About the Merger

Kenny Rocker has articulated Union Pacific’s position on the proposed Norfolk Southern merger with unusual clarity. In his June 7 customer letter, he urges shippers to view the deal not as a typical rail consolidation, but as a competition story focused on single-line service, faster transit, and a stronger challenge to truck freight. Kenny Rocker’s customer letter.

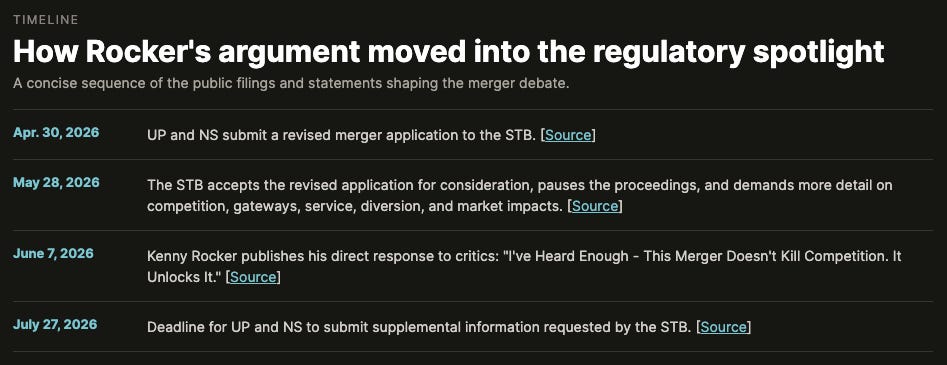

This is timely because the Surface Transportation Board has accepted the revised UP-NS merger application, but paused the formal review and requested supplemental information by July 27 on competition, shipper access, diversion analysis, service assurance, gateways, market share, downstream impacts, and passenger rail. Regulators have made it clear: the case is active, but evidence is still required. STB announcement.

What Happened

Rocker’s letter directly addresses critics who claim the Union Pacific-Norfolk Southern merger would reduce competition and limit shipper options. He firmly rejects this view, arguing that opposition to the deal signals competitors recognize a stronger network emerging. As he stated, “The opposition isn’t evidence this merger will harm competition. It’s the clearest proof, yet, that competition is alive and accelerating.” UP-NS article and reported quote.

Rocker cites the CPKC merger as evidence. He notes that when Canadian Pacific and Kansas City Southern formed a single-line north-south corridor, the market responded dynamically: railroads adjusted services and pricing, and Union Pacific had to compete more aggressively. He highlights Schneider National’s shift of Mexico business to CPKC and UP’s subsequent response on price and product. For Rocker, this is not a warning sign, but a demonstration of genuine competition. UP-NS article.

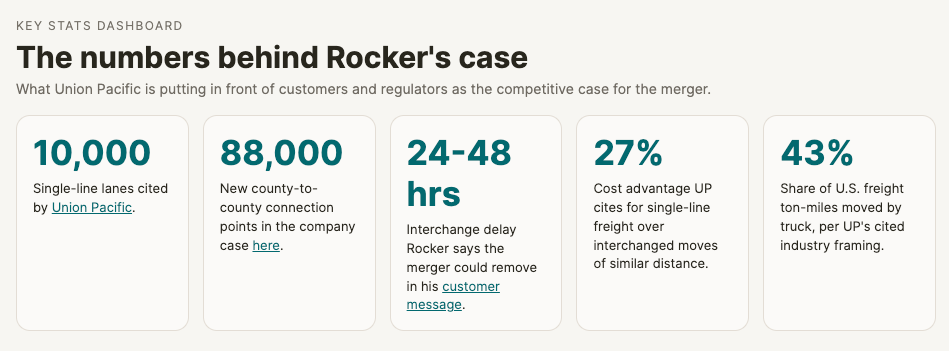

The operational case is particularly relevant for freight executives. Union Pacific states the combined UP-NS network would provide single-line service in 10,000 lanes, connect 88,000 new county-to-county points, add seven new daily intermodal lanes and six new manifest trains, and offer a product that is typically 27% less expensive than comparable interchanged rail service over similar distances, according to economist Mark Israel’s analysis cited by the company. Union Pacific’s June 18 competition case.

Why This Matters

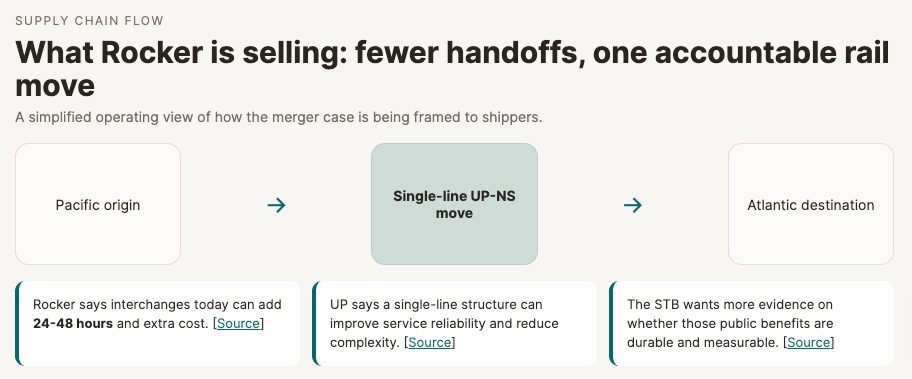

For operators, Rocker’s argument centers on service design rather than merger theory. Eliminating interchanges in a single-line network can reduce handling, decrease variability, improve asset utilization, and provide shippers with a single accountable carrier. Rocker notes that current UP-NS interchanges can add 24 to 48 hours and significant cost to shipments. If validated, this impact is tangible, influencing mode selection, procurement strategy, and network design at the lane level. UP-NS article.

For infrastructure planners, this issue lies at the intersection of physical rail capacity and digital freight management. A transcontinental single-line network changes terminal flows, gateway pressure points, equipment positioning, and standards for end-to-end visibility. This is why the STB is requesting additional information on gateways, car supply, diversion, and service assurance before proceeding to the next phase. STB announcement.

For the broader supply chain, Rocker presents a clear modal argument. Union Pacific notes that trucks handle about 43% of U.S. freight ton-miles, compared to approximately 27% for rail. The company is positioning itself not just as a better railroad, but as a more viable rail alternative in lanes that currently default to highway. This has implications for intermodal strategy, truckload pricing, inland routing, drayage planning, and long-term warehouse placement. Union Pacific competition case and Jim Vena/UP post summary.

There is also an emerging-markets perspective that supply chain leaders should consider. Rocker’s primary historical example is Mexico, which is significant. As North American manufacturing shifts toward Mexico and cross-border freight demand increases, rail networks that enhance north-south and east-west options become more strategically valuable. Rocker emphasizes that network structure is increasingly important as sourcing patterns, industrial geography, and trade flows evolve. UP-NS article.

The Bigger Signal Behind Rocker’s Tone

Rocker’s tone is notable. He does not speak as an executive waiting for the regulatory process to conclude, but as someone convinced that competitive repositioning is already underway. This aligns with Union Pacific’s public statement that competitors have launched new service partnerships since the merger was announced and that railroads are responding even before approval. Union Pacific’s June 18 competition case.

That is why this story matters in the current freight market. Carriers, brokers, forwarders, rail planners, and shippers do not get to wait for the final vote before thinking through network exposure. If a major rail combination changes service maps, freight procurement teams need to know which lanes could become cheaper, which inland nodes could gain relevance, and where truck-rail competition could tighten first. Better freight intelligence is not optional in that environment. It is how operators keep procurement, routing, and margin assumptions from going stale.

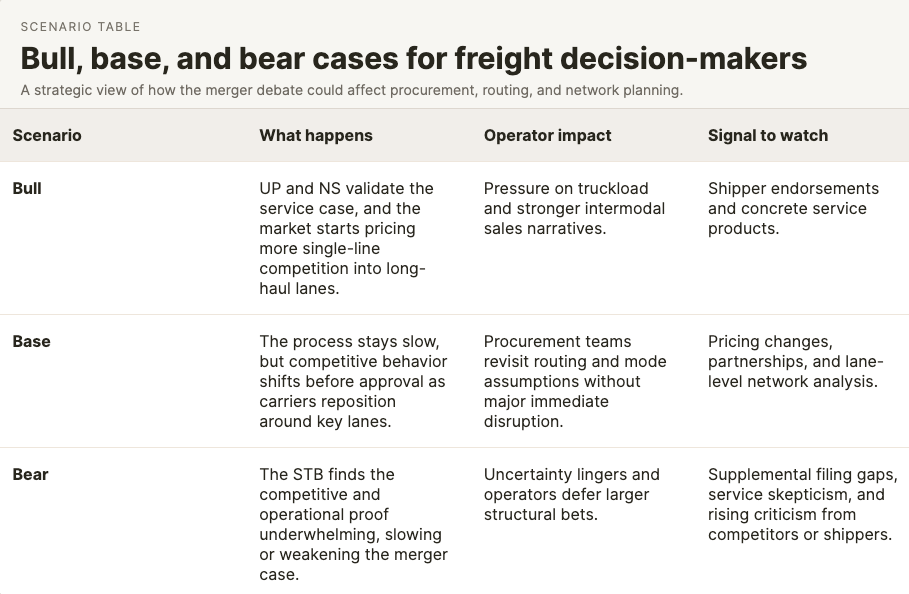

Key insights for decision-makers

Rocker is positioning consolidation not solely as an efficiency measure, but as a competitive tool targeting truck freight and rival rail services, with single-line service as the central value proposition.

The CPKC precedent is central to Rocker’s case. His strongest argument is practical: the last major end-to-end merger prompted competitors to respond and altered pricing behavior.

Infrastructure is a key element of the case. The STB’s request for additional detail on gateways, service assurance, and car supply indicates that operational challenges are as important as the overall narrative.

Mexico remains a strategic indicator. Rocker’s Schneider example underscores the close connection between this debate, cross-border manufacturing, north-south rail competitiveness, and future nearshoring trends.

Mode competition may intensify before any formal approval. Even without a final decision, the prospect of a stronger single-line rail product can affect truck pricing, intermodal sales strategies, and long-term network planning.

What To Watch Next

The next hard deadline is July 27, when Union Pacific and Norfolk Southern must submit supplemental information to the STB on the very issues that sit at the center of Rocker’s case: competition, service reliability, gateway treatment, diversion from truck, and market impact. STB merger decision and STB announcement.

In the interim, the most valuable indicators will be shipper endorsements, competitor responses, service and product changes, and the effectiveness of UP's and NS's substantiation of Rocker’s claims with operational evidence. For freight executives and investors, the key question is not the merger’s controversy, but whether the market is already adjusting to competition before regulatory review concludes.

For teams aiming to stay ahead of these changes, enhanced cost visibility and detailed lane-level insights are crucial. As the network structure shifts, the companies that succeed are often those that identify the cost impacts early. Tools like FreightFA integrate seamlessly into this strategy, serving not just as noise, but as valuable tools to validate assumptions before they affect the P&L.