Amazon’s expansion into broader LTL service is significant. Combined with the FedEx Freight spin-off, the Supreme Court’s broker-liability ruling, and tightening carrier capacity due to ELD and English-language enforcement, these developments signal a market reset rather than isolated events.

For executives, investors, brokers, carriers, and operators, the message is clear: capital, compliance, and data are now central to freight strategy. The market favors scale and strong governance while increasing challenges for less-regulated, low-cost operators.

The landscape has shifted rapidly.

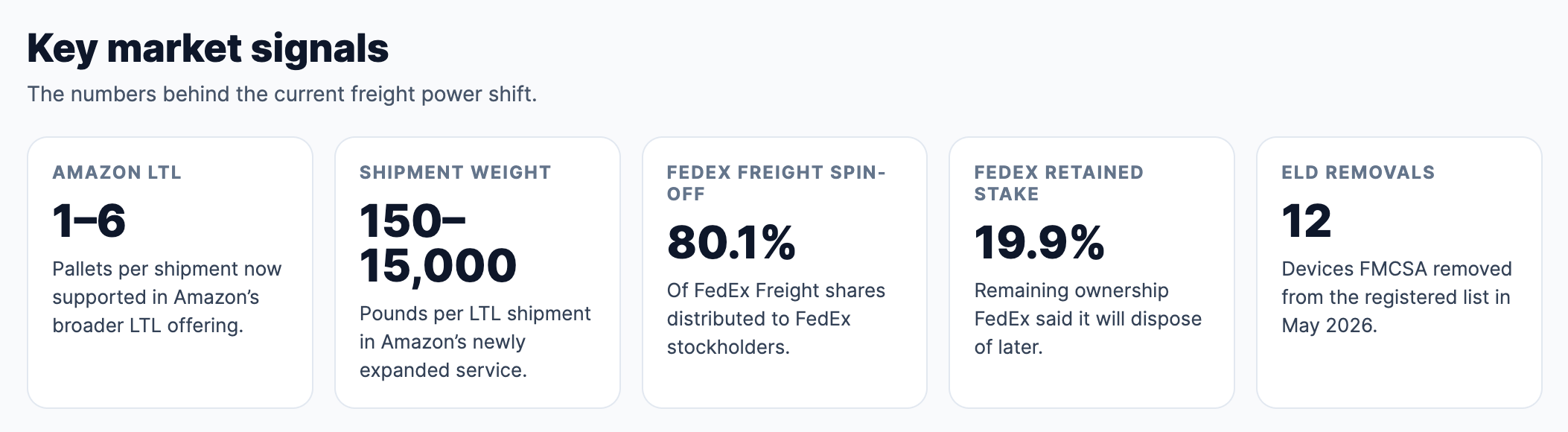

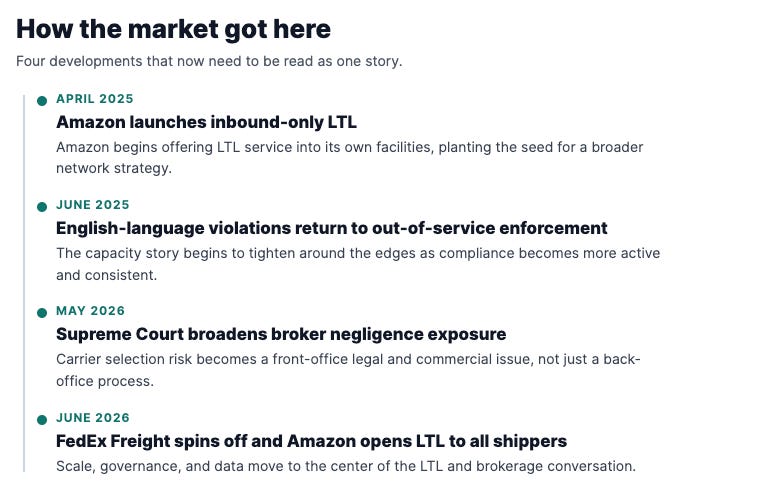

Amazon has expanded its LTL service beyond inbound freight to Amazon facilities and now also includes shippers moving palletized freight between their own sites, retail partners, warehouses, and distributors. Amazon says the service now supports shipments of one to six pallets, roughly 150 to 15,000 pounds, and includes next-day live pickups, same-day drop-trailer pickups, and online quoting and tracking through its portal.

This development is sufficient to alter LTL pricing discussions. Shippers gain an additional branded option featuring familiar technology, broad visibility, and a network that complements Amazon’s truckload and supply chain services. As Amazon stated, “Now, that same standard extends to LTL freight.”

At nearly the same moment, FedEx completed the spin-off of FedEx Freight, establishing it as an independent public company under the ticker FDXF. FedEx CEO Raj Subramaniam called the separation “a pivotal milestone,” adding that it positions “two independent companies to lead their respective industries and create long-term value.” FedEx distributed 80.1 percent of FedEx Freight’s shares to FedEx shareholders and retained 19.9 percent to dispose of later.

The North American LTL market now faces two major strategic shifts: Amazon’s expansion and FedEx Freight’s emergence as an independent, pure-play LTL business.

The legal environment has become more challenging.

The market shift involves both increased competition and heightened risk.

In May, the Supreme Court’s Montgomery ruling reshaped broker liability by opening the door to state-law negligent-hiring claims against freight brokers rather than broadly insulating them under FAAAA preemption. Legal analysis following the decision says the ruling exposes brokers to greater liability when they select unsafe carriers and will likely increase scrutiny around carrier vetting, supervision, and documentation.

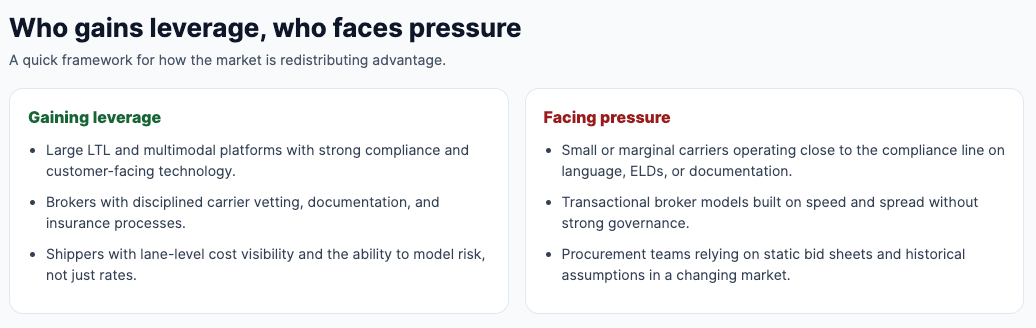

This significantly impacts brokerage economics. Choosing the lowest-cost carrier is now a legal consideration, not merely a margin decision.

Strong operators can manage these changes. However, transaction-heavy broker models with limited carrier oversight face direct risks. Industry value will increasingly favor brokers demonstrating disciplined carrier selection, robust insurance practices, and effective risk controls.

Capacity is not collapsing, but it is gradually decreasing.

Supply dynamics are also evolving. Beginning June 25, 2025, FMCSA enforcement once again made English-language proficiency violations an out-of-service issue nationwide. The Transportation Department said drivers who fail to comply with longstanding English-language requirements will be placed out of service. Separately, FMCSA has continued to remove non-compliant ELDs from its registered list, including the May 2026 removal of 12 devices that carriers must replace before July 20, 2026.

This is not a sudden drop in capacity but rather a gradual tightening at the market's margins.

FreightWaves warned in 2025 that stricter English-language enforcement could strain trucking capacity, increase tender rejections, and push rates higher. By late 2025, trucking executives were already describing the effect as a “slow bleed out,” with capacity exiting through bankruptcies, downsizing, and enforcement of English-language and visa rules.

This shift affects carrier accessibility. Small operators with minimal compliance are increasingly difficult to source, insure, and defend in legal proceedings.

What ties these threads together

This is where the situation becomes more complex.

Amazon’s LTL expansion coincides with a period when large, documented, tech-enabled networks hold structural advantages. FedEx Freight’s separation further emphasizes this by providing investors and customers with a dedicated LTL platform featuring distinct capital structure and strategic priorities. The Supreme Court ruling increases the cost of weak broker governance, while ELD and language enforcement raise the cost of inadequate carrier compliance.

Put together, those forces are pushing freight toward the same destination:

Bigger, cleaner, more transparent networks.

More disciplined carrier selection.

More demand for rate visibility and scenario planning.

Fewer “cheap and loose” options when demand tightens.

This trend affects not only truckload and brokerage, but also warehousing strategy, procurement design, modal selection, and network planning.

The operating implications are broader than LTL

Carriers benefit from investing in compliance, visibility, and customer-facing technology. A strong service offering now includes not only timely pickup and delivery, but also comprehensive documentation, tracking, safety standards, and seamless integration with shipper workflows.

For brokers, the message is sharper. Carrier onboarding, monitoring, and selection are moving from back-office process to front-office differentiation. Brokerages that still rely on fragmented vetting and tribal knowledge are carrying more legal and commercial risk than they did a quarter ago.

For shippers and procurement teams, the trade-off is increasingly clear. Large platforms may not secure every lane, but they offer compelling advantages in risk management, consistency, and integration. These factors will become more important in RFPs, as transportation teams must justify network decisions based on resilience and governance, not just price.

For investors, the capital markets perspective is notable. The FedEx Freight spin-off provides clearer insight into LTL economics, while Amazon tests its ability to attract freight demand through a broader platform strategy. This will likely increase the premium on companies that are scalable, compliant, and analytically mature.

The global angle should not be ignored

While this story is centered in North America, its implications run wider.

As sourcing patterns shift, particularly in Mexico, Southeast Asia, and other manufacturing growth regions, freight networks must address routing complexity, modal transitions, compliance, and inventory positioning across longer, more volatile supply chains. Amazon’s expansion into broader freight services and the market’s preference for larger, governed networks align with these demands.

Infrastructure remains critical. Physical assets such as terminals, trailer pools, warehousing, and intermodal connections are important, but digital infrastructure—including quoting systems, tracking portals, EDI, compliance records, and pricing intelligence—is now equally central in determining competitive success.

That is one reason better cost visibility matters more than ever. In a market where competitive pressure, legal exposure, and capacity quality are shifting at the same time, decision-makers need more than historical averages. They need live context on lanes, modes, and market direction. That is where tools like FreightFA fit naturally into the workflow, not as a pitch, but as a practical response to a market that is getting harder to read by instinct alone.

Key signals for decision-makers

LTL competition is becoming more strategic. Amazon is expanding its supply chain platform into a segment that prioritizes density, reliability, and technology, rather than simply adding another service line.

FedEx Freight now has a cleaner mandate. As a standalone company, it can be judged and managed as an LTL pure play rather than as one unit inside a broader parcel and express portfolio.

Broker compliance now directly impacts valuation. The Montgomery decision increases the cost of poor carrier selection and may distinguish disciplined broker models from those focused primarily on transactional margins.

Capacity quality is tightening. ELD removals and English-language enforcement are not eliminating supply overnight, but they are reducing the easy availability of marginal capacity.

Data is now integral to operations. Rate intelligence, scenario planning, and network visibility are essential components of freight execution, not merely planning tools.ning support.

What to watch next

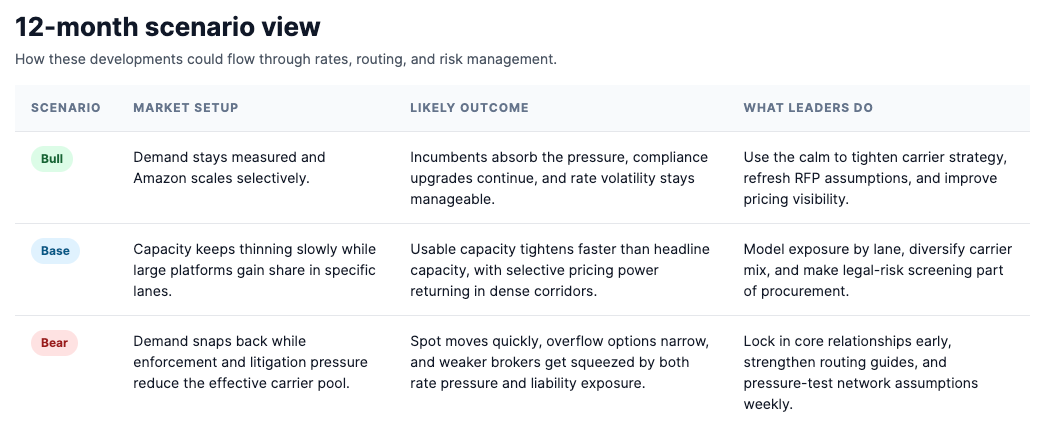

First, watch how aggressively Amazon prices into target lanes and customer segments. If it selectively undercuts incumbents in dense corridors while pairing LTL with broader service offerings, it could influence shipper expectations well beyond its initial share.

Second, observe whether FedEx Freight leverages its independence through improved capital allocation, commercial positioning, or network messaging. As a pure-play public LTL company, it will be expected to demonstrate value creation promptly.

Third, monitor changes in insurance and brokerage practices following the Montgomery ruling. The effects will likely appear first in underwriting, carrier-selection policies, and customer contract terms before impacting broader market data.

Finally, watch the gap between apparent capacity and usable capacity. The market may still look adequately supplied on the surface, but if more of that supply becomes operationally or legally unattractive, pricing power can tighten faster than broad indices suggest.

The freight market is not just becoming more competitive; it is becoming more selective. In this environment, success favors those with strong network discipline, pricing intelligence, and operational credibility.

If you run a fleet, a brokerage, or a supply chain P&L, this is the moment to pressure‑test your network and your carrier list — not just your spot rate sheet.

At FreightFA, that’s exactly what we’re helping teams do with Freight Flow Advisor chat: lane‑level cost estimates, LTL vs TL vs rail trade‑offs, and “what if Amazon/FedEx…” scenario runs in minutes, not weeks.