This quarter, the FMCSA (Federal Motor Carrier Safety Administration) removed several ELDs (Electronic Logging Devices) from its approved list. ELDs are devices that connect to a truck’s engine to automatically record driving time, engine hours, and location, replacing paper logs.

Mandated by the FMCSA, ELDs ensure compliance with Hours of Service (HOS) rules, improve safety by reducing fatigue-related accidents, and expedite roadside inspections. The CVSA (Commercial Vehicle Safety Alliance) also updated its out-of-service criteria. Additionally, Congress included an English Language Proficiency provision in a recent spending bill. These are significant compliance updates.

However, this perspective overlooks the broader impact.

In reality, these actions represent a coordinated regulatory effort that is accelerating the exit of marginal carriers at a pace unmatched by the freight recession alone. Despite three years of low rates, record bankruptcies, and the loss of 122,000 drivers, oversupply persists, with the market still 33% above pre-pandemic carrier authority levels. Economic forces alone have not resolved the issue.

Deciphering the Enforcement Escalation

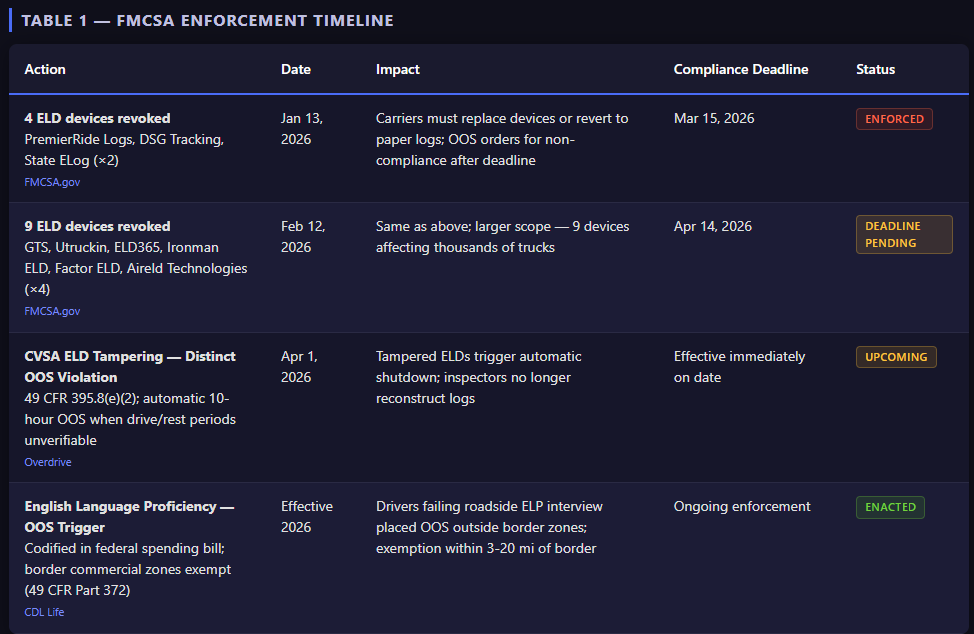

The ELD revocations began on January 13, when the FMCSA removed four devices from PremierRide Logs, DSG Tracking, and State ELog, giving carriers 60 days to replace them or face out-of-service orders starting March 15. On February 12, the FMCSA revoked nine additional devices, including those from GTS, Utruckin, ELD365, Ironman ELD, Factor ELD, and all four Aireld Technologies devices, with a replacement deadline of April 14.

That’s 13 ELD devices revoked year-to-date across 8 distinct ELD providers. FMCSA Administrator Derek D. Barrs put it plainly: “If an ELD isn’t meeting federal requirements, it’s taken out of service — plain and simple.”

In effect, devices selected by budget carriers for their low cost, minimal compliance, or ease of manipulation are being systematically removed. Each revoked device may impact hundreds or thousands of trucks. Carriers using these devices must either invest in a compliant replacement within 60 days or cease operations. For small owner-operators with narrow margins after three years of recession, even a $400–$600 ELD replacement, along with downtime and reconfiguration, can threaten their business.

Additionally, effective April 1, the CVSA’s 2026 out-of-service criteria update classifies ELD tampering as a distinct violation under 49 CFR 395.8(e)(2), separate from traditional false-log violations under (e)(1). This distinction is significant.

Previously, inspectors had some discretion with false-log violations. If they could estimate the driver’s actual driving and rest periods, even from altered logs, the out-of-service calculation could be adjusted. While still a violation, trucks could often return to service relatively quickly.

The new tampering rule eliminates flexibility. If an inspector finds a tampered ELD with erased editing history—a log Jeremy Disbrow called “a work of fiction”—the driver gets a 10-hour out-of-service order. No negotiation or chance to reconstruct drive or rest periods. Oregon DOT has enforced this, using a fuel receipt to show an ELD was altered for at least three days, resulting in a fabricated log and immediate removal.

English Language Proficiency is now also a factor. Under a provision in the recent federal spending bill, failing an ELP (English Language Proficiency) assessment results in an out-of-service order. The FMCSA has confirmed that commercial zones along the U.S.-Mexico border, as defined under 49 CFR Part 372, subpart B, are exempt. However, in all other areas, if a driver cannot pass the interview portion of a roadside ELP assessment, the vehicle must be taken out of service.

These policies might seem like routine compliance updates but collectively they set a regulatory baseline preventing freight market oversupply. All enforcement measures target undercapitalized, non-compliant operators who historically re-enter when rates improve—this pathway is now closing.

Supply Destruction Data

The enforcement escalation is landing on a market that was already hemorrhaging capacity.

According to revised BLS (Bureau of Labor Statistics) data reported by Land Line Media, the trucking industry has lost 122,000 drivers since October 2022. In 2025 alone, 28,000 drivers left the industry, eight times the initial estimate. This represents a significant exodus rather than normal attrition.

In January 2026, there were 20 carrier bankruptcy filings, setting a record for a single month. Tractor builds declined by 32% from the first to the second half of 2025, indicating that OEMs (Original Equipment Manufacturers) do not anticipate a near-term capacity rebound.

NTI’s (National Transportation Institute) 2026 Driver Market Forecast reports a 5% decline in the for-hire interstate driver segment by the end of 2025, indicating an accelerating loss of capacity. The average driver age is 46, and the BLS projects 237,600 annual job openings through 2034 will be needed to maintain current capacity.

As of February 2026, there are still 342,487 carriers with active authority, which is 33% above pre-pandemic levels. While oversupply persists, it is being reduced more rapidly than at any previous point in the current downcycle.

On the rate side, DAT (DAT Freight & Analytics) reports a seventh consecutive monthly increase in spot rates. The national spot van average is now $2.41 per mile. C.H. Robinson has raised its full-year forecast to a 12% year-over-year increase. The recovery is now evident in market data.

Meanwhile, the LTL (Less-than-Truckload) sector lost 5,000 jobs in a single month, reaching its lowest employment level since November 2014, excluding the COVID-19 period. The impact is not evenly distributed; it is concentrated among operators already struggling, many of whom now face ELD revocations, stricter log requirements, and English proficiency assessments at weigh stations outside border zones.

For shippers evaluating carrier partners, these figures serve as an early warning. Any carrier on your approved list that has not confirmed ELD compliance, or that relies on drivers in areas with active ELP enforcement, represents a capacity risk that could disappear with little notice.

The Carrier Verdict: “Tailwind”

This perspective is not limited to analysts; carriers themselves are acknowledging it.

In the Q4 2025 earnings roundup compiled by CCJ (Commercial Carrier Journal), multiple major carriers explicitly cited regulatory enforcement as a positive force for rate recovery:

Knight-Swift CEO Adam Miller noted that capacity reduction from stricter regulatory enforcement was driving market tightening.

Marten Transport CEO Randolph L. Marten highlighted stricter CDL (Commercial Driver’s License) standards and English Language Proficiency enforcement as expected to “positively impact growth opportunities to reduce capacity.”

Werner Enterprises Chairman and CEO Derek Leathers cited ongoing regulatory capacity attrition as a “supportive tailwind.”

Covenant Logistics executives pointed to regulatory enforcement as “an emerging tailwind to accelerate capacity exits and help restore rate momentum.”

In summary, the largest and most compliant carriers in the United States are publicly stating to shareholders that current regulatory actions are benefiting their businesses.

What They’re Missing: The Structural Thesis

Most coverage treats these developments as separate issues: ELD revocations, ELP enforcement, and bankruptcy filings. However, this approach overlooks their combined impact.

The new regulatory baseline prevents the typical market reset. In previous freight downcycles, low rates attracted new entrants due to inexpensive authority, affordable ELDs, and minimal barriers. Now, the FMCSA is eliminating low-cost ELDs, the CVSA is enforcing stricter log requirements, and Congress is requiring drivers to communicate effectively with inspectors. As a result, marginal entrants who would have returned at $2.00 per mile spot rates in 2019 are unable to do so in 2026.

These exits are permanent. A carrier that loses its ELD, cannot afford a compliant replacement, and faces an April 14 deadline will likely cease operations. Similarly, a driver placed out-of-service for ELP failure who lacks resources to address the issue will leave the industry. Unlike demand-driven capacity exits, where trucks may sit idle but authority remains active, regulatory exits are final.

Investments in compliance now serve as a significant competitive advantage. Carriers that invested in Tier 1 ELD platforms, English language training, and safety departments are seeing competitors removed from the market through regulatory action. This advantage grows with each new FMCSA revocation notice. For compliant carriers, investments made during the downturn are now yielding returns through reduced competition. The market is not only rewarding compliance; regulatory agencies are actively enforcing it.

The Excess Capacity Argument

The primary counterargument is the current authority count. With 342,487 carriers, the market remains 33% above pre-pandemic levels. This represents substantial excess capacity, and regulatory enforcement has historically been slow, inconsistent across jurisdictions, and subject to political changes. A new FMCSA administrator, shifts in Congressional priorities, or legal challenges from ELD manufacturers could slow enforcement.

Uncertainty exists whether displaced capacity truly leaves the market or reorganizes. An owner-operator losing authority might lease to a larger carrier, and a driver out-of-service for ELP may get work with a border zone company. Some exits may not be permanent appear.

Additionally, the rate recovery, though real, remains fragile. The current spot van rate of $2.41 per mile is still well below the $3.00-plus peaks of 2021-2022. Demand-side risks such as tariff uncertainty, reduced consumer spending, and inventory destocking could stall the recovery, regardless of supply-side developments.

Regulation Is Doing What the Market Couldn't

Over the past three years, the freight recession reduced capacity through bankruptcies, rate compression, and driver attrition, resulting in the loss of 122,000 drivers and 20 carriers in a single month. Despite these reductions, the market remains oversupplied.

Now, the FMCSA is implementing measures that economic forces could not achieve: establishing definitive, non-negotiable exit triggers. These include 13 ELD revocations, an April 1 tampering crackdown with automatic out-of-service orders, and an ELP enforcement regime codified by Congress. Surviving carriers view these changes as a positive development.

When considering the regulatory escalation, the loss of 28,000 drivers in 2025, tractor builds 32% below replacement levels, and seven consecutive months of spot rate increases, the evidence supports a thesis not widely discussed: the rate recovery is driven not only by demand, but by supply reduction, with regulatory action as the catalyst.

The key question is whether this trend will continue. If the current pace of enforcement is maintained, it is likely that it will.

Want these insights wired into your quoting process, not just your inbox? Get instant LTL, FTL (Full Truckload), Rail, and intermodal rate intelligence at FreightFA. See what the platform can do!