The mainstream narrative is that the Panama Canal has fully recovered from its historic drought, with reservoirs refilled, 38–40 daily transits, and full draft limits restored. In contrast, the Suez Canal is effectively closed following U.S.-Israeli strikes on Iran, triggering another major carrier rerouting around the Cape of Good Hope. This is often framed as good news for Panama and bad news for Suez—two separate stories in different oceans.

These are not separate issues. Together, they are reshaping global container shipping economics in real time—and the outcomes differ sharply from most analysts’ expectations.

The Panama Miracle, by the Numbers

February 2026 was the wettest month in the Panama Canal’s 132-year history. Alajuela is at roughly 99% capacity and Gatun above 90%. The Canal Authority even executed preventive water discharges after Gatun Lake reached its 88.93-ft maximum operational level — a dramatic reversal from just two years ago, when the canal was rationing transits and slashing draft limits due to record drought (Newsroom Panama).

Operationally, Panama is back to full strength. Neopanamax draft limits are restored at 50 feet, Panamax locks at 39.5 feet, and daily transits at 38–40 — essentially full capacity. For transpacific shippers, especially Asia–U.S. East Coast, this is a clear win: vessels move without delay, slot availability is healthy, and the 2023–2024 congestion premium has disappeared.

But this recovery story is incomplete. Panama’s rebound is happening as another major chokepoint effectively closes, and the interaction between these events is now driving freight rates and capacity in ways a canal-by-canal view cannot explain.

The Suez Shutdown — Again

On March 1, Maersk, Hapag-Lloyd, CMA CGM, and MSC—three of the four largest container carriers globally—simultaneously suspended Suez transits and rerouted vessels around the Cape of Good Hope. All four also halted crossings in the Strait of Hormuz, representing a complete operational withdrawal rather than a limited precaution.

The Strait of Hormuz data shows the severity. On March 10, Windward tracked just two commercial crossings — both outbound, zero inbound — versus a seven-day average of 3.29. Over nine days, only 66 vessels transited what is normally one of the busiest shipping corridors on earth.

Even before this escalation, Suez traffic was weakening. January 2026 saw just 150 container ship transits — the weakest January in a decade, down 16.7% year-over-year (Global Maritime Hub). A tentative return of carriers through the Red Sea in late 2025 — with over 70% of diverted traffic back on Suez routes by January — has now completely reversed (Gosships).

The Cape reroute adds ~19 days to westbound Asia–Europe transits and ~7 days eastbound. That time penalty cuts annual cargo throughput per vessel on affected routes by 10–15%. Industry analysts estimate $2–3 billion per week in additional carrier operating expenses (Gosships).

The Rate Divergence Nobody’s Pricing Correctly

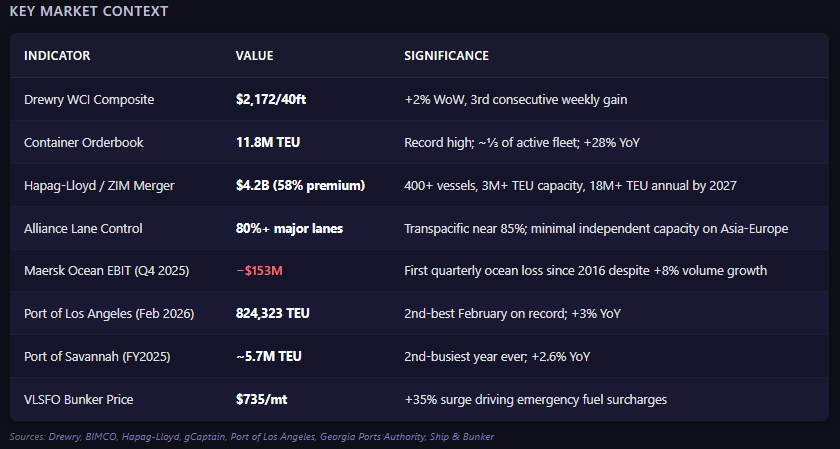

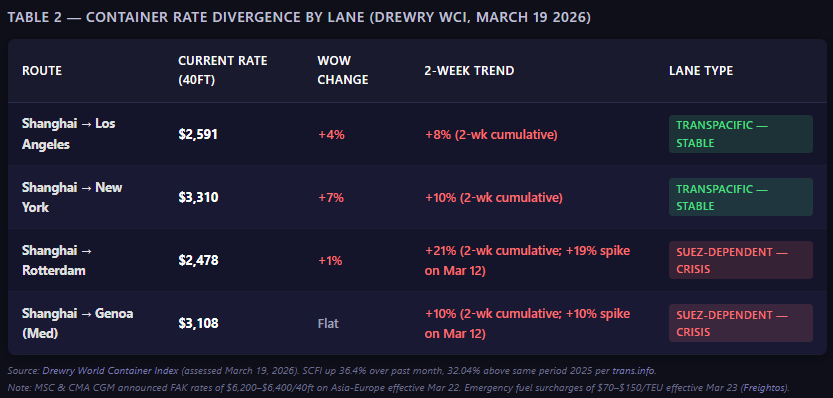

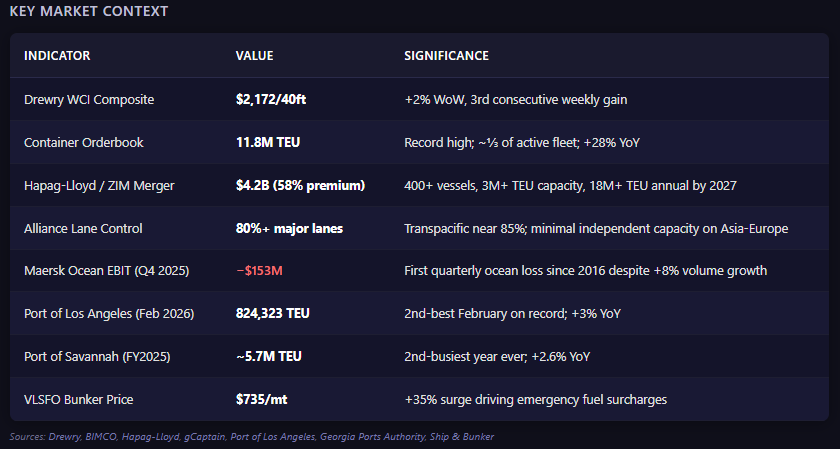

The latest Drewry World Container Index (March 19) shows the composite at $2,172/40ft, up 2% and marking a third consecutive weekly gain. But that single number hides a widening fault line between lanes:

Transpacific lanes — Panama-accessible, Suez-independent:

• Shanghai–Los Angeles: $2,591 (+4% WoW)

• Shanghai–New York: $3,310 (+7% WoW)

Asia–Europe lanes — Suez-dependent, now Cape-routed:

• Shanghai–Rotterdam: $2,478 (+1% WoW, +19% two weeks prior)

• Shanghai–Genoa: $3,108 (flat WoW, but +10% two weeks prior)

The transpacific is rising on normal seasonal demand patterns. The Asia-Europe corridor experienced a violent 19% weekly spike in Shanghai-Rotterdam rates when the rerouting hit, followed by carrier announcements of FAK (freight-all-kinds) rates of $6,200-$6,400/40ft from MSC and CMA CGM, effective March 22 (Container News).

Meanwhile, the SCFI is up 36.4% over the past month, running 32.04% above the same period in 2025. CMA CGM and Hapag-Lloyd have layered emergency fuel surcharges of $70-$150/TEU effective March 23, driven by VLSFO prices surging over 35% to $735/mt (Freightos; Ship & Bunker).

Transpacific shippers see modest seasonal rate hikes, while Asia-Europe shippers face surcharges, high spot rates, and Cape rerouting costs, highlighting market disparity.

Asia-USEC lane shippers via Panama enjoy stable conditions, full draft access, and predictable transit times. Conversely, shipping to Europe or the eastern Mediterranean adds three weeks, new fuel surcharges, and FAK rates nearly triple current spot rates. Though supply chains and carriers are similar, cost structures now differ significantly..

The 2024 Playbook Doesn’t Work This Time

Referring to 2024 precedent might seem tempting. When Houthi attacks forced carriers around the Cape, rates surged and surcharges rose, but the situation normalized in about six months. By late 2025, over 70% of diverted traffic returned to Suez routes, showing system resilience.

However, the 2024 analogy has limits. First, the threat has changed. Houthi attacks posed targeted risk, while U.S.-Israeli strikes on Iran create systemic risk affecting the Strait of Hormuz, a route for 20% of global oil. This shifts the issue from routing to energy, impacting bunker costs..

Second, the financial position has changed; early 2024 saw carriers holding pandemic-era cash reserves, but now Maersk reports quarterly losses. The industry expects rate compression in 2026 due to oversupply, not rerouting costs. Third, consolidation has shifted; the Hapag-Lloyd/ZIM deal was previously unannounced, and alliances were more competitive. Now, capacity concentration on major lanes limits independent routing options during disruptions.

The Alliance Chokepoint

Now layer in the consolidation dynamics. Hapag-Lloyd’s $4.2 billion acquisition of ZIM — at a 58% premium — will create a combined entity with over 400 vessels, capacity exceeding 3 million TEU, and annual throughput above 18 million TEU by 2027 (Hapag-Lloyd; ZIM Investors).

Alliance-controlled carriers now hold over 80% of major lane capacity, with transpacific concentration approaching 85%. When three of the top four carriers suspend Suez transits simultaneously, this reflects coordinated action within an oligopoly rather than a typical market adjustment. Independent capacity on Asia-Europe routes is extremely limited, and alliance scheduling decisions highly influence the spot market

The merger timeline is also significant. Until the deal closes, expected in late 2026, Hapag-Lloyd and ZIM remain separate competitors, but the market is already anticipating reduced competition. After the merger, the combined fleet’s high proportion of chartered tonnage—over 86% of ZIM’s fleet is chartered—will allow Hapag-Lloyd to adjust capacity across lanes as needed (Czapp).

What They’re Overlooking: The Oversupply Dilemma

The key insight is that these factors make forecasting for 2026 particularly challenging.

The orderbook was supposed to fix this. The global container orderbook stands at a record 11.8 million TEU — roughly one-third of the active fleet — up 28% year-over-year. In 2025 alone, owners ordered a record 4.8 million TEU of new capacity. Shipowners ordered another 665,000 TEU in just the first two months of 2026 (BIMCO). The consensus entering the year was that this flood of new tonnage, combined with a return to Suez routes (which would release ~6% of global fleet capacity, according to Zencargo), would crush rates in 2026.

The Suez closure just created a split market. On transpacific lanes — which benefit from the fully operational Panama Canal and don’t depend on Suez — the oversupply thesis still holds. Rates are elevated but manageable. The Port of Los Angeles processed 824,323 TEU in February, its second-best month ever, up 3% YoY (Port of LA). Savannah handled nearly 5.7 million TEU in FY2025 (Georgia Ports Authority). Cargo is flowing.

On Suez-dependent lanes, there is an artificial capacity shortage. The addition of new vessels does not offset the fact that each ship now requires an extra 19 days per round trip. The fleet is effectively reduced by 10-15% on these routes, even as the total number of ships reaches record levels. As a result, oversupply and undersupply are occurring simultaneously on different lanes within the same ocean.

What are the next steps from this point?

The freight market now has two distinct parts, connected by the same carriers but diverging by lane. This makes single-number rate forecasts ineffective. Transpacific lanes remain stable due to Panama Canal access, while Asia-Europe and Asia-East Coast routes face rising rates, surcharges, and more increases signaled by carrier FAK announcements.

For 3PLs, margin models should incorporate lane-level detail rather than relying on broad benchmarks. BCOs with European distribution should plan for 50-60 day transits instead of 30-40 days. Those in truckload or intermodal should watch for secondary effects, as USEC port volumes may shift if Panama absorbs more Asia-USEC cargo, possibly changing drayage and inland distribution.

Alliances, which control over 80% capacity, rely on the continued use of single-number market views to set prices and surcharges by lane. A more granular approach is advisable.

Want these insights wired into your quoting process, not just your inbox? Get instant LTL, FTL, Rail, and intermodal rate intelligence at FreightFA. See what the platform can do!