The freight market is advancing up the value chain. As brokerage margins remain under pressure and global supply chains become more compliance-driven, capital-intensive, and network-dependent, large 3PLs are shifting toward 4PL-style orchestration. They are bundling customs, warehousing, technology, and financing into a unified operating layer.

This shift is significant for executives, investors, and operators because it alters the location of profit pools, determines ownership of shipper relationships, and influences which platforms will be essential in the next cycle.

The setup

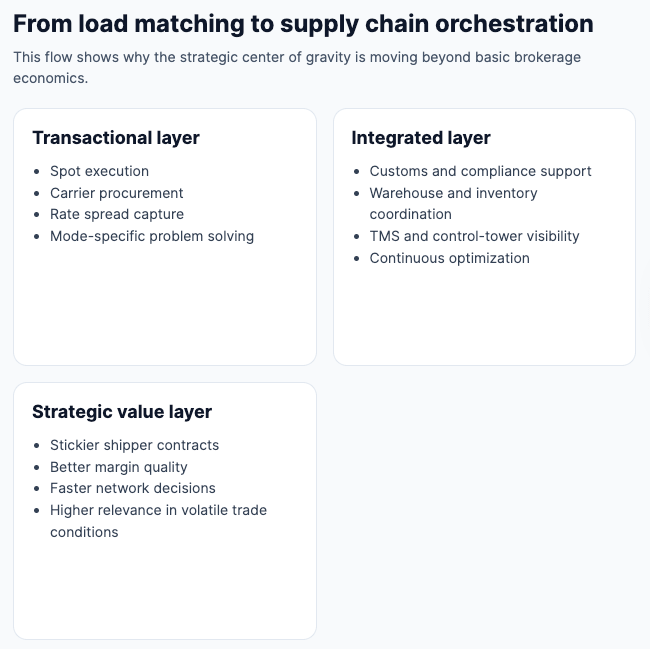

Historically, much of logistics value came from execution and transaction spreads: booking capacity, managing exceptions, and capturing margins. While this model remains relevant, it is less defensible as digital rate visibility increases and shippers seek greater control over cost, compliance, and working capital.

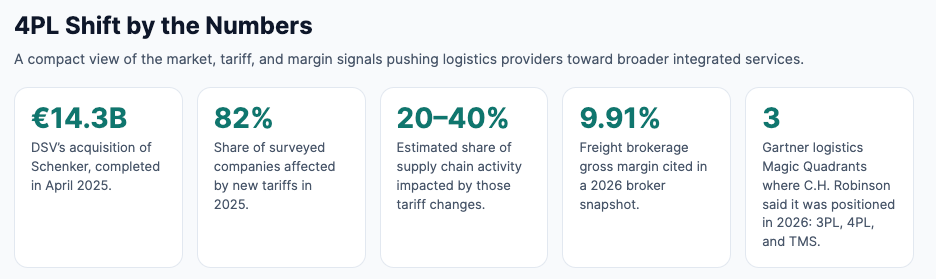

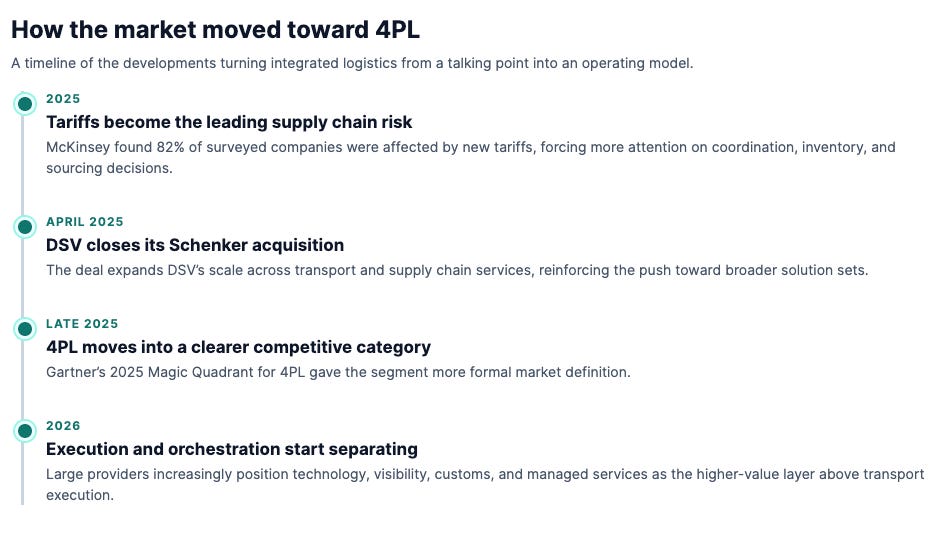

Meanwhile, the largest logistics providers are expanding and integrating further. DSV completed its acquisition of Schenker in April 2025 for approximately EUR 14.3 billion. The combined company aims to grow by enhancing service offerings and leveraging economies of scale. Deutsche Bahn described the transaction as giving DB Schenker “a new owner that promises a unique market position and opportunities for international growth.”

This language is important. The consolidation is not solely for scale, but to build a broader service stack around freight.

What happened

The main trend is clear: many large 3PLs are consolidating, scaling, and adopting integrated service models that increasingly resemble 4PLs. These models offer end-to-end orchestration across transport partners, planning tools, freight settlement, customs support, warehousing coordination, and performance management.

: Company Profile, Stock Price, News, Rankings | Fortune")

C.H. Robinson has embraced this approach. Gartner named the company a Leader in its 2025 Magic Quadrant for Fourth Party Logistics. C.H. Robinson states its 4PL model is based on “true supply chain orchestration,” end-to-end visibility, AI maturity, global scalability, and continuous optimization for cost and performance. In March 2026, the company reported it was the only provider positioned across Gartner’s three logistics-related Magic Quadrants for 3PL, 4PL, and TMS categories.

Market conditions also support this shift. McKinsey found that 82 percent of surveyed companies reported their supply chains were affected by new tariffs, with 20 to 40 percent of supply chain activity impacted. With significant exposure to tariffs, customs, and sourcing volatility, shippers now prioritize coordination over isolated truck moves.

Where the value is moving

Margin quality is the clearest indicator. Freight brokerage remains sizable, but transaction-driven economics are increasingly difficult to defend as capacity procurement becomes more transparent and rate volatility narrows spreads. FreightWaves reported an average broker gross margin of 9.91 percent in a 2026 industry snapshot. FreightCaviar noted that gross margins declined from above 16 percent in Q2 2023 to just above 15 percent in Q1 2025 among top public brokers.

This does not mean brokerage will disappear. Instead, standalone brokerage becomes more comparable and easier to replace. Greater value now lies in coordinating modes, managing data, handling customs challenges, improving inventory positioning, and reducing shipper decision time across the network.

This explains the growing use of 4PL terminology. According to C.H. Robinson, a 4PL partner serves as the connective tissue across regions, partners, systems, and workflows. This integration enhances pricing power, increases contract retention, and positions carrier execution as part of a broader solution rather than the sole value proposition.

Why does this matter on the ground?

For carriers, brokers, and forwarders, this shift is tangible. It directly influences purchasing decisions, freight awards, and which operators maintain leverage.

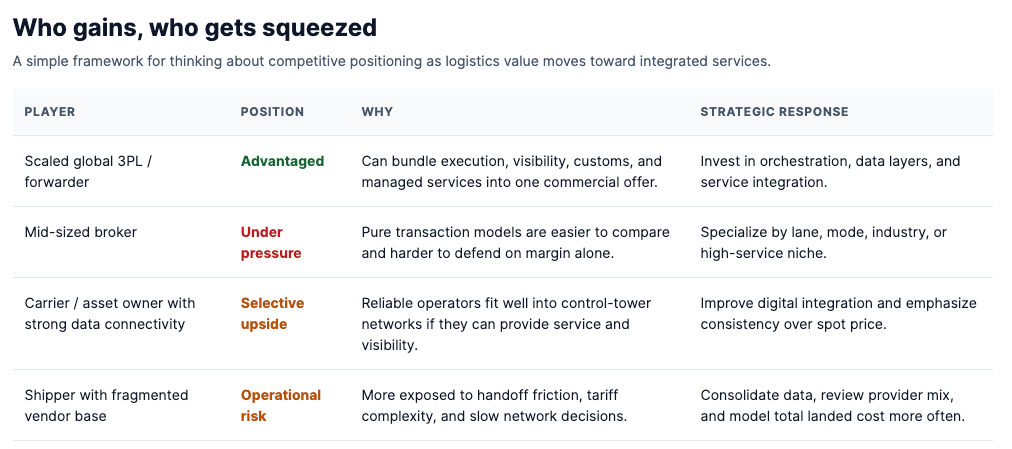

Shippers dealing with tariff exposure, customs delays, variable inventory turns, and pressure to reduce landed costs do not want multiple disconnected vendors and competing dashboards. They seek a single operating layer that can model scenarios, manage disruptions, connect warehouse and transport decisions, and make cost-service tradeoffs visible in real time.

This shift is reshaping the hierarchy within the freight ecosystem:

Large 3PLs and forwarders gain a competitive edge by combining orchestration with execution.

Mid-sized brokers are under pressure to specialize by mode, lane, vertical, or service intensity if they cannot scale into integrated offerings.

Asset owners and carriers increase their value by integrating with control-tower models that reward reliability, visibility, and network fit, rather than focusing solely on the lowest price.

In summary, while the load remains important, the network decision surrounding the load is now more critical.mckinsey+1

The emerging market angle

This shift also has global implications. Tariff pressure, supplier diversification, and nearshoring are leading companies to redesign supply chains across Mexico, Southeast Asia, India, and other manufacturing growth markets. McKinsey found that 39 percent of tariff-exposed respondents were pursuing dual sourcing, and 33 percent were developing supplier nearshoring or onshoring plans. mckinsey

This creates opportunities for logistics providers to develop new corridors instead of serving only legacy routes. Growth in emerging production hubs increases demand for customs expertise, inland connectivity, multi-country warehousing strategies, and cross-border visibility. Providers capable of coordinating drayage, air, ocean, customs, and distribution across evolving sourcing maps are positioned to capture a larger share of business.

For investors, this is one reason integrated platforms attract more strategic attention than pure-play intermediaries. These platforms are linked not only to freight volumes but also to supply chain redesign.

Infrastructure is back in the center.

The shift toward 4PL-style models also places physical and digital infrastructure at the center of logistics competition. Ports, rail ramps, cross-docks, bonded facilities, warehouse automation, TMS layers, control towers, AI-based exception management, and customs systems are now integral to the commercial equation.

This has two implications. First, operators with substantial infrastructure or strong access to it become more strategic when combined with effective orchestration software. Second, infrastructure alone is insufficient when tariff exposure and routing volatility change frequently.

The likely winners will be those who combine both: hard assets or dense execution networks, and high-velocity planning intelligence.

Signals for decision-makers

A few signals stand out for executives reading this market:

Monitor whether large brokers continue to focus on loads or shift their language toward control towers, orchestration, and managed services. Such vocabulary changes often signal an impending shift in revenue mix.

Evaluate M&A activity based on service adjacency, not just scale. The DSV-Schenker deal is significant because it expands integrated reach across modes and supply chain services, not merely due to its size.

Expect customs and compliance to become central to commercial operations. Tariff volatility is turning regulatory competence into a key revenue driver. mckinsey

Expect improved data to become a margin-generating product. Visibility into true network costs, service tradeoffs, and procurement options is increasingly part of the service offering, not just an internal tool. chrobinson

This highlights the growing importance of freight intelligence. As logistics value shifts from execution to network orchestration, decision-makers require tools that quickly clarify costs, routing, and exposure. Platforms focused on freight cost visibility and market context, such as FreightFA, are well-suited to this environment because they help teams interpret volatility rather than simply react to it.

What to watch next

The next phase of this story will likely show up in three places.

First, more large providers will formalize managed-service offerings using 4PL terminology, regardless of whether they fully rebrand their models. Second, shipper procurement decisions will increasingly focus on resilience, customs capability, and network flexibility rather than transportation price alone. Third, mid-market intermediaries will face greater pressure as customers seek broader solutions and fewer handoffs.

For freight leaders, the strategic question is becoming clearer: are you selling a movement, or are you helping customers manage their supply chains? In today’s market, lasting value is found in the latter.

Want to see where freight rates and market conditions are heading as this 4PL shift plays out?

FreightFA gives shippers, brokers, and logistics operators instant access to AI-powered freight rate estimates, market intelligence, and supply chain cost visibility — all in one platform. Stop guessing. Start moving smarter.